Delve into the complexities and significance of Loss Contingency within the realm of intermediate accounting with this complete information. Improve your understanding as you discover its definition, and the vital role it holds in accounting. Discover the step-by-step process for accounting for loss contingencies, its journal entries and GAAP tips. Get a real-world perspective with frequent enterprise situations, while additionally debunking widespread misconceptions.

If vital to the financial statements, provisions for estimated losses are proven as a separate legal responsibility on the stability sheet. The contract provision would generally be proven as a contract cost on the income statement. The steadiness sheet method (also generally recognized as thepercentage of accounts receivable method) estimates bad debtexpenses based on the balance in accounts receivable. The stability sheet technique isanother easy technique for calculating unhealthy debt, but it too does notconsider how long a debt has been outstanding and the position thatplays in debt recovery.

📹 How Much Do You Stroll Away With Out Of Your Settlement?

- In GAAP accounting, it means the defendant pays the plaintiff a sum of cash to stop the lawsuit.

- At the end of the year, the accounts are adjusted for the actual warranty expense incurred.

- This account ought to be both revenue or expense, primarily based on the settlement sort.

- Nevertheless, the expense and related reimbursement could also be netted in revenue or loss underneath each IFRS and US GAAP.

- When a balance of funds deficit or surplus occurs, inflows or outflows of reserve belongings bring the ledger again into balance, recorded in the official settlement account.

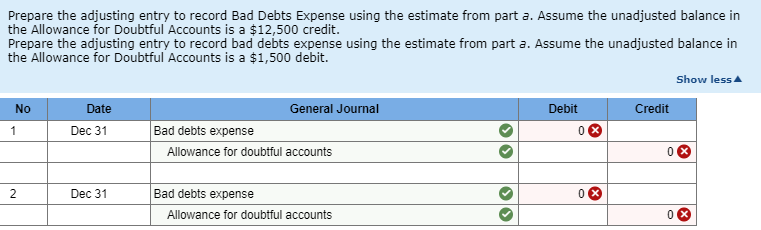

The allowancemethodestimates dangerous debt throughout a interval, based mostly oncertain computational approaches. When the estimation isrecorded at the finish of a period, the following entry happens. The ultimate level pertains to https://www.simple-accounting.org/ firms with very little exposureto the chance of dangerous debts, usually, entities that rarelyoffer credit score to its customers. Assuming that credit just isn’t asignificant element of its sales, these sellers can also use thedirect write-off methodology. The companies that qualify for thisexemption, nonetheless, are usually small and not main participantsin the credit score market.

Understanding The Definition Of Settlement

The direct write-off method delays recognitionof unhealthy debt till the specific customer accounts receivable isidentified. Once this account is identified as uncollectible, thecompany will report a discount to the customer’s accountsreceivable and a rise to bad debt expense for the precise amountuncollectible. Contingent liabilities can negatively affect a company’s belongings and net earnings. However, if the probabilities of a contingent liability are attainable however not prone to come up quickly, estimating its value is not potential. Such loss contingencies by no means get recorded in the financial statements, but full disclosure should be made in the footnotes.

Accounting Requirements Codification (ASC) 606, Income from Contracts with Clients, doesn’t particularly handle loss contracts. Instead, guidance for loss contracts is present in ASC 605 and in other ASC matters. This article brings these topics together as a useful resource for figuring out the accounting for loss contracts. The allowance method is the extra broadly used technique because itsatisfies the matching precept.

Two traditional examples of contingent liabilities embody a company guarantee and a lawsuit towards the corporate. Both symbolize possible losses and both depend on some unsure future event. On the balance sheet, an organization records a settlement liability if a loss is likely and may be estimated. This legal responsibility exhibits the company’s future obligation to pay the settlement. When the payment is made, the legal responsibility decreases, and the payment is shown in the money flow assertion.

Thus, virtually all the remaining unhealthy debtexpense materials mentioned here will be primarily based on an allowancemethod that makes use of accrual accounting, the matching principle, andthe revenue recognition rules underneath GAAP. If a contingent legal responsibility meets these two criteria, will most likely be journalized and recorded as a loss or expense within the statement of revenue and loss, and a liability in the balance sheet. To document a contingent liability in financial statements, it must clear two fundamental criteria based mostly on the probability of prevalence and its corresponding worth. If an organization can fairly estimate the value of guarantee claims based on historic data, they should document a warranty legal responsibility. If the company can fairly estimate the value of guarantee claims primarily based on historical data, it ought to report a guaranty liability. These types of liabilities require cautious accounting treatment to make sure accurate financial reporting and to prevent potential monetary dangers.

There is another point about the usage of the contra account,Allowance for Doubtful Accounts. In this instance, the $85,200 totalis the web realizable value, or the quantity of accounts anticipatedto be collected. Nevertheless, the company is owed $90,000 and willstill attempt to acquire the whole $90,000 and never just the$85,200. 401(k) plans and pensions frequently offer vested advantages when employers contribute.

Usually Accepted Accounting Ideas

From contract inception by way of December 31, 2021, Company ABC recorded $125,000 in income over time primarily based on the formulation below. The recognition of a gain contingency isn’t allowed, since doing so might result within the recognition of income earlier than the contingent event has been settled. The Corporate is subject to numerous authorized proceedings, claims, and regulatory actions arising within the ordinary course of enterprise. The outcomes of those matters are inherently unpredictable, and the Firm intends to defend itself vigorously towards all claims.

The assessment considers all available proof, together with post-reporting date events and some other precedents. Disputed liabilities can have an effect on a company’s credit rating if they result in delayed payments, defaults, or legal judgments. Credit companies may view unresolved disputes as indicators of financial instability or poor vendor relations. Even if the legal responsibility is contested, failure to handle it proactively can negatively influence the company’s perceived creditworthiness.